{kind=link}

{kind=link}

Jim Tobin, A Friend Of Liberty (1945-2021)

May 2nd, 2022

By: Christina Tobin

Sometimes a single man or woman has to stand up for principle, just so t[...]

ALBANY—Taxpayers United of America (TUA) today revealed retired government employee pensions for the County of Albany, New York’s state government retirees, and statewide government teachers. Many New York government employees are becoming pension millionaires when retired.

“Many government retirees make more in pension payments than the private sector taxpayers make in salaries,” stated Christina Tobin, TUA Vice President.

“According to the Empire Center, ‘NYSTRS and NYSLRS are ‘fully funded’ by government actuarial standards, but we estimate they have combined funding shortfalls of $120 billion when their liabilities are measured using private-sector accounting rules’. Pension liabilities continue to be the number one budgetary concern for states, counties and municipalities,” added Tobin.

“I have hand delivered a letter to Gov. Cuomo and will mail the Legislature, calling for additional pension reform that will be both fair and sustainable. TUA is ready to work with legislators to implement reforms that will preserve the system for those that are relying on it, and bring relief to the taxpayers who are obligated to fund it.”

“Private sector New Yorkers are struggling in the ‘Great Recession,’ with an average personal income of $36,000.

The unemployment/underemployment rate (U6) is 14.9%, and New York State is still the second highest tax state in the country. The maximum Social Security annual payout is $22,000, regardless of how much one may have earned in their working career.”

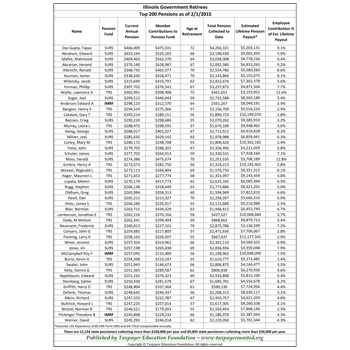

“William E. Carl, retired Albany County government employee, collects an annual pension of $77,423. His estimated lifetime payout is $2,903,379.*”

“Phillip W. Wood, retired from the State University of New York, has an annual pension of $186,295 with an estimated lifetime payout of $6,986,069*.”

“Retired New York teacher, James H. Hunderfund, has a lifetime estimated payout of $11,859,188* based on his actual annual pension of $316,245.”

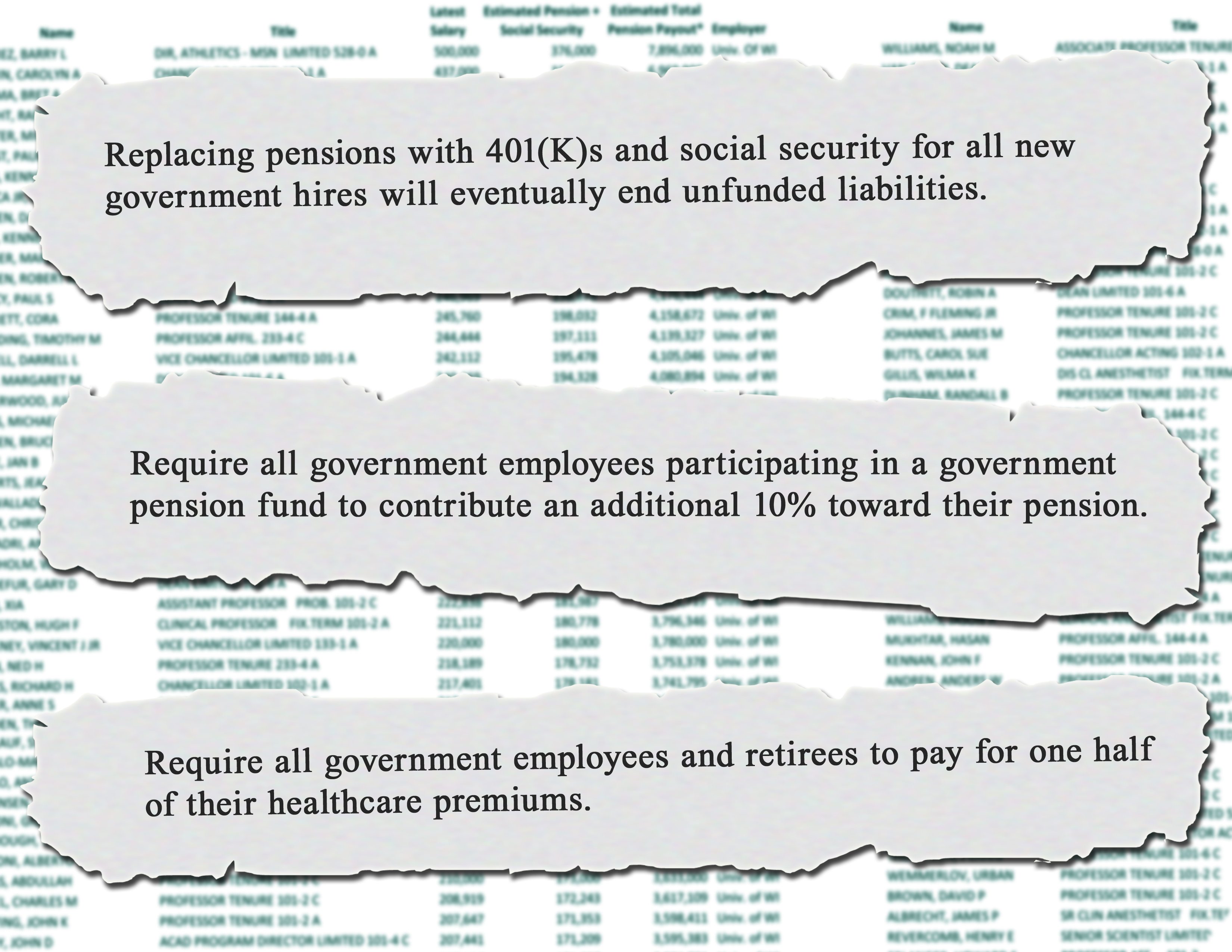

“New York government pension systems are making millionaires out of public employees at taxpayer expense. Replacing defined benefit pensions for all new government hires and with social security and 401(k)s would eventually eliminate unfunded government pensions. If current government employees would just increase their pension contributions, they would preserve their pension benefits. Anything less will not ensure benefits for those counting on them. We need a stable system that is fair to both taxpayers and beneficiaries.”

“Every employee deserves a fair wage for the work they do at the time they do it so they can plan for their own retirement, rather than counting on the bureaucrats who helped create such an unstable situation.”

“This is the time for the political courage to do what’s in the best interest of taxpayers, rather than the special interests. Let’s knock any politician out-of-office, who cuts deals with bad union bosses and bad corporations! Republican or Democrat, what’s the difference, with numbers like these?”

View pension amounts below:

*TUA submits FOIA requests for actual pensions. Since personal information is not available, lifetime pension payouts must be estimated based on retirement at 55, life expectancy of 85 (IRS Form 590), and 1.5% COLA.

Thanks a lot for providing individuals with such a marvellous chance to read in detail from this web site. It’s usually very lovely and as well , full of a good time for me personally and my office mates to visit your web site at the least three times in one week to learn the fresh items you have got. And of course, I’m just actually pleased for the eye-popping inspiring ideas you give. Certain 2 ideas in this post are in fact the simplest I’ve ever had.