Jim Tobin, A Friend Of Liberty (1945-2021)

May 2nd, 2022

By: Christina Tobin

Sometimes a single man or woman has to stand up for principle, just so t[...]

Christina Tobin, Vice-President of Taxpayers United for America, was featured in yet another WISH-TV 8 story on Indiana’s growing pension problem.

Updated: Wednesday, 16 Nov 2011, 8:23 PM EST

Published : Wednesday, 16 Nov 2011, 8:21 PM EST

Troy Kehoe

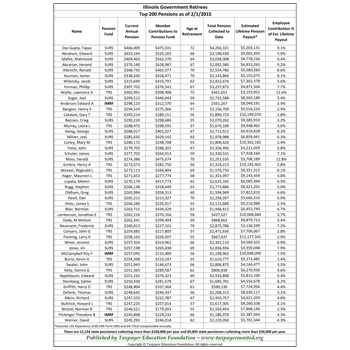

INDIANAPOLIS (WISH) – A national taxpayer rights group came to Indiana on Wednesday, armed with figures it says shows your tax dollars are being spent on what it calls “lavish” pensions.

The news conference by executives from Chicago’s Taxpayers United of America (TUA) came just one day after I Team 8 exposed details of a state law keeping more than $2 billion in annual pension payouts confidential from the taxpayers who fund them.

“The real issue here is that, in Indiana, they don’t release the pensions. There needs to be more transparency in Indiana. There definitely is not enough,” said TUA Vice President Christina Tobin.

Because Indiana law prevents the public release of pension payout information, the group says it estimated those payouts instead. Its estimates include university administrators, coaches, professors, judges, teachers and other public employees. TUA says its findings show hundreds of the state’s current top salary earners could get total lifetime payouts that reach into the millions of dollars after they retire.

“The pension payouts are so high, if we don’t reform the pensions, we’re going to have serious issues, not just in Indiana, but nationwide,” Tobin said.

But some aren’t convinced.

TUA’s estimations assume employees will retire at the age of 55, under their current salary, after remaining in their current position for at least 30 years.

Because not all on the estimated list will fit those assumptions, some say the group’s numbers are far too high. Under Indiana law, most of the state’s retirement funds require at least 10 years of service to be vested. Some on the list have not even satisfied that requirement yet.

Asked by 24-Hour News 8’s Troy Kehoe if high pension payments to individual public retirees are contributing to the state’s $14 billion shortfall in pension funding , IUPUI Professor Dr. Craig Hartzer shook his head.

“No,” he said. “When you look at other states and you look at the average annual benefit that our retirees are getting, that’s not going to be an issue.”

Hartzer served as director of Indiana’s Public Employee Retirement Fund (PERF) for more than 20 years.

“In fact,” he continued, “I think we need to do a better job of letting people know that the average retirement benefit in our state is extremely low. And pay tends to be lower for the same kinds of education levels. I think the pensions in the public sector are designed to retain public employees, because you don’t get vested until at least 10 years of service.”

According to retirement system documents obtained by I Team 8, the average pension benefit given to a retired public employee in fiscal year 2010 was around $19,500, though the average benefit from the state’s seven separate retirement funds was closer to $24,000. The state also claims only about 1,700 retirees – or about 1 percent – get more than $36,000 in pension benefits per year.

But Tobin argues there’s no way to prove that because the state’s confidentiality law prevents the public from seeing hard data to back up the state’s claims.

“In other states where we do get pension information, the majority of those individuals do get 20-30 year payouts. These are estimates. That’s the best we can do,” she said.

Hartzer agreed that lifting at least some of the curtain of secrecy on the system might help remove some suspicion.

“Maybe it could be a bit more transparent than it is today,” he said. “But I do think the information is there. I think it’s more helping people find the information they’re looking for.”

Tobin remains convinced the state should go even further.

“We want pension reform, is what we want. We aren’t saying to take away the pensions. We’re asking for them to put more money into the system so it’s less of a burden on the taxpayers,” she said.

The group is calling on Indiana legislators to end fully funded state pensions for all new government hires, replacing it with a “401k-style” defined contribution plan.

“If each current government employee were required to contribute an additional 10 percent toward his or her pension, taxpayers would save billions of dollars,” TUA said in a news release.

Others say that would take away benefits the state has already promised, and without the proper education, some worry forcing employees to manage their own investments could be problematic.

“Some of these are going to be very, very drastic and difficult answers to what we’re looking for,” said Rep. David Niezgodski, D-South Bend, a member of the General Assembly’s Pension Management Oversight Commission. “But, what happens 20 years down the line if we do all these things, and now everyone is completely without? That becomes maybe our problem again.”