Jim Tobin, A Friend Of Liberty (1945-2021)

May 2nd, 2022

By: Christina Tobin

Sometimes a single man or woman has to stand up for principle, just so t[...]

Jim Tobin, President of Taxpayers United for America, was interviewed by WISH-TV 8 on Indiana’s growing pension problem.

Updated: Friday, 11 Nov 2011, 6:27 AM EST

Published : Thursday, 10 Nov 2011, 11:00 PM EST

Troy Kehoe

INDIANAPOLIS (WISH) – Nearly half-a-million Hoosiers are counting on getting a state pension when they retire. It’s a promise Indiana made to everyone from teachers and police officers to city snow plow drivers and county clerks. But, a two-month I Team 8 investigation uncovered serious concerns over the funding used to issue those pension checks, and some say you could be forced to help pick up the bill to fix it.

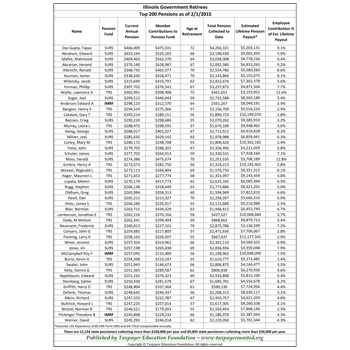

Indiana’s retirement system is one of the largest in the country, with assets approaching $26 billion. With so much money at stake, I Team 8 wanted to find out just how healthy and reliable those funds are.

After months of investigation, we found the answer comes down to simple math, and an equation that’s making a growing number of baby-boomers increasingly apprehensive.

Not Making the Grade

Standing in front of the blackboard inside her classroom at Shortridge High School, Alene Smith is fulfilling a lifelong dream every day.

“I teach law and court process, and I also coach track. This is my 23rd year of teaching,” she told 24-Hour News8, smiling from ear to ear.

“Teaching is a calling,” Smith continued. “Last year, I said this is the most fun I’ve ever had. This year, I’m saying this is the most fun I’ve ever had. It truly is a calling. It’s just such a great profession!”

It’s supposed to be a great profession with a great retirement plan. In addition to various annuity options, most public employees have a state funded pension—funded solely by taxpayers, and given to retirees with at least 10 years of service.

But, I Team 8 has found the fund used to pay for some teachers’ pensions isn’t making the grade.

It’s a warning signal pension experts like IUPUI’s Dr. Craig Hartzer have been studying for years. Hartzer ran Indiana’s Public Employee Retirement Fund (PERF) for more than 20 years; before it was combined with the state’s six other retirement funds in 2010. All seven funds are now overseen by the newly formed Indiana Public Retirement System (INPRS).

“Five years ago when I left [PERF], it might have been around $8 billion in unfunded liabilities. Today it might be [closer to] $15 billion,” Hartzer said.

Asked if those figures set off a new set of alarm bells, Hartzer nodded.

“If I were a retired teacher, and I had to depend on the Indiana General Assembly to make appropriations out of the general fund to cover my retirement check, I’d be worried,” he said.

That’s because–for 75 years—teachers used what the state called a “pay-as-you-go” pension system. While teacher pension payments were guaranteed by the state, no money was set aside through their paychecks or from their schools in order to make their payments. Lawmakers simply paid each year’s teacher pension bill through the state budget. That changed in 1996, when the General Assembly set up a new fund which accumulates money for future payouts–like other public employees.

According to the latest INPRS actuarial report, that new teachers retirement fund—now known as TRF 96–contains 94.7 percent of the funding it needs to pay out all of its members, though many of them won’t retire for decades. But, for teachers like Smith who were hired before 1996, the state’s “pension bank” is much more dire. Those same figures show the “Pre-96 TRF funded at only 33.1 percent–about $11 billion short of its obligations.

How could that happen?

“We are looking at dire straits because certain people in the legislature–or the entire legislature–didn’t do their job right,” said Rep. David Niezgodski (D-South Bend). “I hate to say it, but I think promises were made and promises were not kept.”

Still, despite that lack of funding, more than 45,000 baby boomer teachers hired under the “old” system have already cashed in on their promised benefits, and nearly 25,000 more will likely do the same within the next 20 years. That’s only increasing the shortage.

A New Budget Battle

At the latest meeting of the General Assembly’s Pension Management Oversight Commission, its Chairman Sen. Greg Walker (R-Columbus) said the growing problem could put future state budgets in jeopardy.

“No, I’m not comfortable,” he said when asked if enough was being done to address the issue. “I think we’ve got some good minds looking at this, but our current state across the nation is for some funds to be in default. There have been deferred payments over the years where it’s time to pay the piper. I don’t want to see Indiana get into that same position.”

Neither does Smith.

“It does [worry me],” she said. “Because, I’m one of those teachers that will be retiring in the next 10-15 years, it is a bit frightening.”

And, not just for teachers.

I Team 8 put all seven of Indiana’s retirement funds under the microscope, and found most are thought of as “healthy.”

“Generally speaking, the funds are in very solid condition, ahead of where most funds are

in the nation in terms of funded status,” said INPRS Communications Director Jeff Hutson.

With the exception of teachers–they’re way ahead–for everyone from police officers and firefighters to snow plow drivers, county clerks. Lawmakers aren’t far behind. Take away those baby-boomer teachers from the mix, and Indiana’s retirement funds are 87.5 percent funded. That puts the state in the top ten, with the most money socked away to make pension payments, according to a recent Pew Center for the States study. According to that study, the national average for all funds is 78 percent.

But, add in the Pre-96 TRF fund, and Indiana’s total fund balance drops to just 64.5 percent, leaving the state without a single penny to pay nearly one-third of its eventual retirees.

And, while the other funds are better off than many other states, none has enough money to pay all the members it will eventually owe. Funds used to pay the retirements of judges and prosecutors are of particular concern, as they currently list funding statuses of only 66.5 percent and 53.3 percent, respectively.

Some say the numbers should serve as a call to action.

“If we don’t reform the pensions, there’s going to be a collapse in the system,” said Jim Tobin, Founder and President of Chicago based Taxpayers United of America, one of the largest tax reform groups in the nation.

It’s a problem in other states too, leaving retirement systems across the country on the verge of disaster. The Pew Center estimates states are now more than $1 trillion short of their pension obligations, and only three states—Wisconsin, New York and Washington—have fully funded pension systems.

That’s where you come in.

Because legislators are using the state budget to bail out the underfunded Pre-96 TRF, and your taxes fund the state budget, you’ll have to pay to fix this.

Asked if there are concerns that will contribute to a budget crisis in the future, Niezgodski didn’t hesitate to respond.

“I would think so, if more steps aren’t taken,” he said.

Fixing the system

Indiana—like many other states—is left with three basic options in order to manage that crisis: default on promised payments, make drastic state budget cuts in combination with reserve funding, or raise taxes. The last of the options might not come solely from the state.

Because PERF saw the market value of its assets fall from a peak of nearly $17 billion in late 2007 to about $10 billion in early 2009, the Associated Press reported in September that cities, counties and other local governmental taxing bodies across Indiana will see an 11 percent average increase next year in what they have to toward their employees’ pension funds. While PERF’s market losses have since bounced back to around $15 billion, INPRS Director Steve Russo says higher contribution rates are needed to recover from the investments hit.

That could cause havoc in local budgets, already being hit by a loss in funding from the state’s new property tax caps. While the state of Indiana’s rate is expected to go up by about 23 percent in 2012, the city of Indianapolis will be forced to pay 43 percent more into the pension accounts of its current employees in 2012. That means the city will need to cut an additional $4 million from its upcoming budget, in addition to cuts already being made from its current $64 million budget deficit.

Even that, however, won’t make a complete fix.

A new study from the Franklin Center for Government and Public Integrity suggests every Hoosier household would have to pay an additional $300 in new taxes every year for the next 30 years simply to cover pension payments the state has already promised.

For those like Tobin, that’s an unacceptable burden.

“You’re going to have to work until you drop to pay for this,” he said. “Taxpayers should not be forced to do this, [when] we don’t get pensions in the private sector anymore.”

According to a recent report by the non-profit Manhattan Institute, only 15 percent of Americans are collecting a full private pension, and many companies have frozen or abandoned their pension plans altogether. Tobin says it’s a compelling argument as to why public pensions should be cut…or cut out.

But, state legislators on both sides of the aisle argue—ending the system all together would be unfair too.

“We just can’t throw it out because–well, we didn’t look at it sooner. So, now we’re going to have to hit the employee again? That’s not right,” Niezgodski said.

Walker argues higher public pensions should be viewed as a form of “compensation” for lower wages in the public sector than the private sector.

“I look at pensions as a tool of recruitment for quality talent,” he said.

Some argue pensions are an economic tool, too.

A 2008 study from Indiana University’s Kelly School of Business found approximately 90 percent of all Hoosier pension payments are re-spent within Indiana’s borders, creating more than 11,000 new jobs.

But, if taxes and cuts don’t close the gap, what will?

Some other states are taking a “hybrid” approach, floating proposals to raise mandatory retirement ages from 55 to 65 or even 67. In California, Governor Jerry Brown has called for public employees to raise their contributions to their own pension funds to 50 percent, essentially sharing the burden with state taxpayers.

In Indiana, the solution may be a shift, of sorts. Sen. Brent Waltz (R-Greenwood) plans to introduce a bill in the upcoming legislative session that would require all new hires of the state, schools or local governments, to have a so-called defined-contribution plan—similar to a 401(k)-style plan.

In a pension–or defined-benefit plan—taxpayers guarantee annual retirement benefits for public employees. Defined-contribution plans require workers to contribute to a retirement account, with employers typically offering a matching contribution.

Hartzer worries the switch could put public employees at risk of not having enough retirement savings.

“If you mandate a defined-contribution plan for all new employees, what you’ve done is shifted all the investment risk to the employees, and most employees are not very literate about investments,” he said.

But, Walker argues, with Indiana’s pension deficit growing every day, the state has to look at all its options.

“The government is in volatile investment times with rising benefit costs, rising health care costs and an increasing number of retirees every year,” Walker said. “We need to be talking about how we best protect employees of the state.”